MERSCORP Holdings, Inc. is a privately held corporation that owns and manages MERS System and all other MERS products. It is a member-based organization made up of more than 5,000 lenders, servicers, sub-servicers, investors and government institutions.

MERSCORP

Frequently asked questions

About MERS

What is MERSCORP Holdings?

What is MERS?

Mortgage Electronic Registration Systems, Inc. (MERS) is a wholly-owned subsidiary of MERSCORP Holdings, and its sole purpose is to serve as mortgagee in the land records for loans registered on MERS System. MERS is a nominee for the lender and subsequent buyers (“beneficial owners”) of a mortgage loan and serves as a common agent for the mortgage industry.

What is MERS System?

MERS System is a national electronic database that tracks changes in mortgage servicing rights and beneficial ownership interests in loans secured by residential real estate.

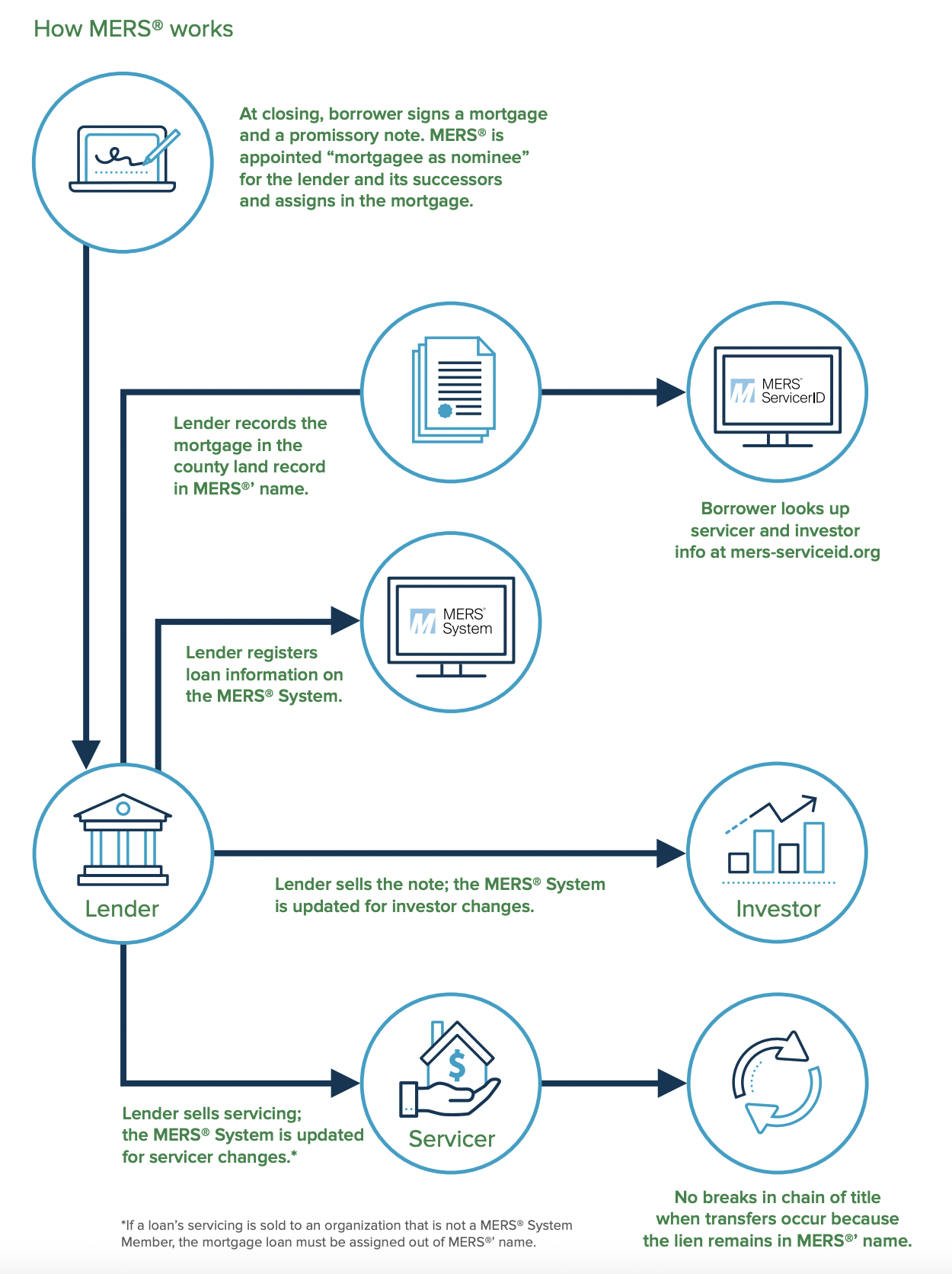

How does MERS work?

What is the MERS eRegistry?

MERS eRegistry serves as the industry's system of record for identifying the owner (Controller) and custodian (Location) of registered eNotes. It enhances liquidity, transferability, and security for lenders by ensuring eNotes are in a secure electronic format. By reducing risk and streamlining processes, it helps lenders generate greater profits and shortens the time between loan closing and securitization, enabling instant movement of eNotes and faster funding.

The MERS eRegistry is one of multiple functions utilized by Participants to satisfy the control requirement of Section 201(c) of the E-SIGN Act and Section 16(c) of the UETA with respect to a transferrable record (“eNote”). Its role is to be the authorized source to identify the party that has Control of the eNote and the Location (i.e., the party that maintains the Authoritative Copy of the eNote). Each Participant is responsible for determining that all the functions, including the MERS eRegistry as set forth herein, utilized by the Participant and its service provider(s) constitute a system that satisfies the control requirements of Section 201(c) of the E-SIGN Act and Section 16(c) of the UETA.

Are MERS loans recorded in the public land records?

All MERS mortgages (or deeds of trust) registered on MERS System are recorded in the public land records. MERS System is not a system of public record, nor a replacement for the public land records. No interests in those mortgages (or deeds of trust) are transferred on MERS System; they are only tracked. MERS as original mortgagee eliminates breaks in the chain of title because the lien is grounded in MERS' name.

How does MERS become a mortgagee or beneficiary?

There are two ways. In most cases, MERS becomes mortgagee or beneficiary at closing when the borrower and lender both agree to standard language in the security instrument making MERS the original mortgagee or beneficiary, with the right to act on behalf of the lender and its successors and assigns. The standard language is approved and used by Fannie Mae, Freddie Mac, Ginnie Mae, the Federal Housing Administration (FHA) and the Veterans Administration (VA). In cases where MERS is not named as the original mortgagee on the security instrument, a lender can record an assignment of the mortgage to MERS after closing.

What does “MERS as original mortgagee” mean to borrowers?

MERS’ role and rights are clearly spelled out in the contract between borrower and lender. When borrowers sign the mortgage security instrument at closing, they agree to standard language that grants and conveys legal title of the mortgage to MERS as mortgagee, giving the company the right to act on behalf of the current and subsequent owners of the loan.

Does MERS collect mortgage payments from borrowers?

No. MERS, MERSCORP Holdings or MERS System do not service mortgages. Mortgage lenders, or other mortgage servicing companies, collect payments from borrowers and manage their loans. Borrowers who have questions about their loans, or who need help with foreclosure prevention, should contact the company they send their payments to - not MERS or MERSCORP Holdings.

Does MERS have the documents for loans registered on MERS System?

No. MERS, MERSCORP Holdings or MERS System are not document custodians and do not hold promissory notes or mortgage documents on behalf of lenders, servicers or investors. We are not responsible for keeping mortgage records - the servicer maintains the loan files.

What does MERS do for lenders?

As the mortgagee of record, MERS receives service of process, legal notices and other mail regarding the mortgaged properties. MERSCORP Holdings, Inc., on behalf of MERS, sorts, scans and transmits documents electronically to the appropriate MERS System Member. Because MERS is a common agent for its members, recording an assignment of the mortgage is eliminated when ownership of the promissory note or servicing rights transfer between members. This reduces work and cost. MERS System also provides information on undisclosed liens, which reduces fraud.

How does MERS benefit borrowers?

MERSCORP Holdings, Inc. provides access to data in MERS System free of charge to homeowners, county officials, and regulatory officials (subject to privacy restrictions). Homeowners can access the data on their mortgage loans registered on MERS System through MERS Servicer ID online or by phone at (888) 679-6377.

Having trouble finding information on our website?

Please contact us.